Tax lien investing has become one of the most discussed alternative real estate investment strategies in the United States. For beginner retail investors looking for passive income, predictable returns, and lower entry costs compared to traditional real estate, tax liens offer a structured and government-backed opportunity that deserves serious attention.

This comprehensive guide explains everything beginners need to know about tax lien investing, including tax lien certificates, auctions, redemption periods, risks, laws, and beginner strategies. It is designed to serve as a pillar resource for investors exploring tax lien investments through platforms like Unified Tax Liens (UTL) and educational systems such as Tax Lien Wealth Builders, MarketPlacePro.net, and Unified Wealth System.

Throughout this guide, you will find educational explanations, strategic insights, and practical steps to help you understand how tax lien investing works and how it fits into a real estate investment portfolio.

For a deeper understanding of real investor experiences and platform credibility, you can review it here.

What Is a Tax Lien?

Understanding tax liens is the foundation of tax lien investing. Before exploring auctions, certificates, and strategies, investors must clearly understand what a tax lien is and why it exists.

Tax lien definition

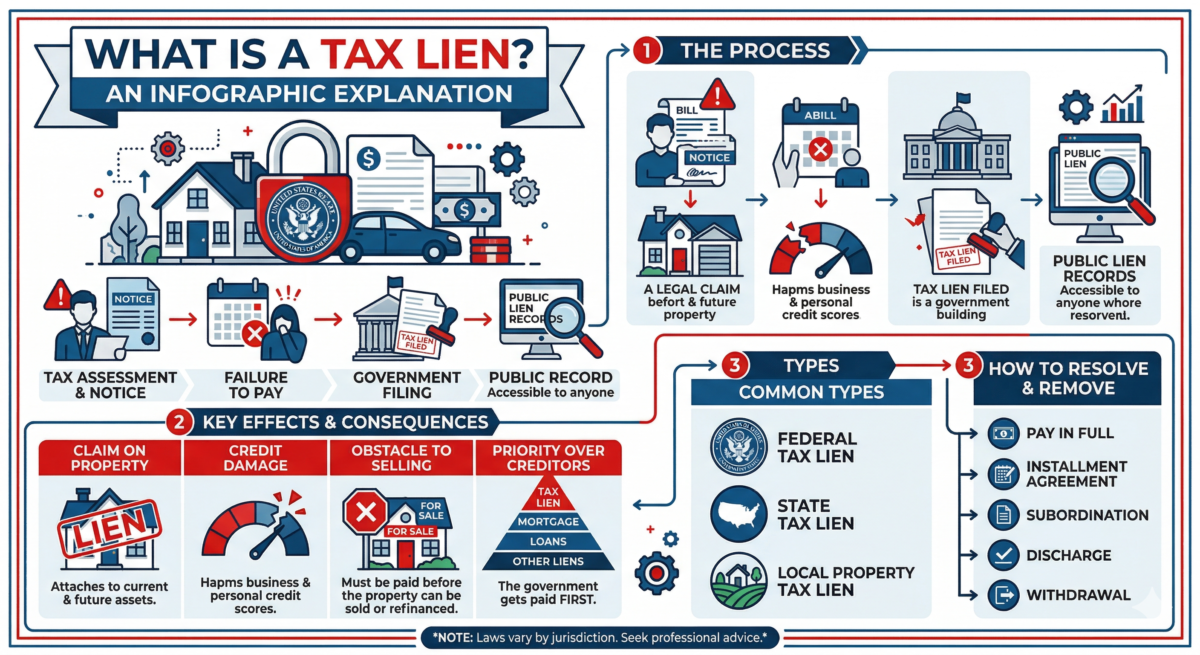

A tax lien is a legal claim placed by a government entity on a property when the owner fails to pay property taxes. The lien ensures that the government has a legal right to collect unpaid taxes, interest, and penalties before the property can be sold or refinanced.

In simple terms, a tax lien acts as a secured debt attached to real estate. The local government does not immediately take the property, but it records a legal claim against it until the debt is paid.

IRS explanation of tax liens

Learn how tax lien opportunities are structured in real investment environments at United Tax Liens.

Tax lien meaning in real estate

In real estate, a tax lien represents a priority claim against a property. This means that the lien must be resolved before ownership can be transferred, mortgages refinanced, or other legal actions completed.

For investors, this is important because tax liens are typically senior to mortgages and many other types of debt. That priority position makes tax lien certificates a unique type of real estate-backed investment.

Tax liens do not automatically transfer property ownership. Instead, they create a legal claim that can generate interest income or lead to foreclosure if the owner does not pay.

To understand how tax lien investments compare with other real estate strategies, explore MarketPlacePro.

What does a tax lien mean for property owners

For property owners, a tax lien is a serious financial and legal issue that can significantly affect their ability to manage, refinance, or sell their property. When property taxes remain unpaid, the local government places a legal claim on the property, known as a tax lien, which must be resolved before the owner can regain full financial control of the asset.

This situation creates several important consequences that property owners need to understand.

Key consequences of a tax lien

A tax lien creates multiple financial and legal restrictions that grow more severe over time if the debt is not resolved.

The property cannot be sold easily

One of the most immediate consequences is the difficulty of selling the property. Since the government holds a legal claim, any buyer or lender will require the lien to be cleared before the transaction is completed. This often delays sales or discourages potential buyers altogether.

Refinancing becomes difficult

Lenders typically avoid financing properties with existing tax liens because they represent a high financial risk. As a result, property owners may struggle to refinance their mortgage or secure new loans, limiting their financial flexibility.

Interest and penalties accumulate

Tax liens usually carry fixed interest rates and penalties that continue to grow over time. The longer the taxes remain unpaid, the larger the total debt becomes, turning a relatively small tax obligation into a significant financial burden.

The risk of foreclosure increases

If the unpaid taxes are not resolved within the legal timeframe, the government or the tax lien certificate holder may initiate foreclosure proceedings. This can ultimately lead to the loss of the property, making tax liens one of the most serious consequences of unpaid property taxes.

Credit and financial stability may be affected

A tax lien can negatively impact a property owner's financial standing, making it harder to obtain loans, invest in other properties, or maintain long-term financial stability.

The redemption period explained

Most jurisdictions offer property owners a redemption period, which is a legally defined timeframe during which they can repay the unpaid taxes along with interest and penalties.

How the redemption period works

During this period, the property owner still retains ownership and has the opportunity to clear the debt. Once the taxes and fees are fully paid, the lien is removed, and the property returns to good standing.

This redemption period is what creates the investment opportunity for tax lien investors, as they earn interest while property owners work to repay their obligations.

Why governments issue tax liens

Local governments depend heavily on property taxes to fund essential public services and maintain community infrastructure. Without consistent tax revenue, cities and counties would struggle to operate effectively.

Essential services funded by property taxes

Property tax revenue supports critical services that communities rely on every day.

Schools and education

Public schools and educational programs rely on stable tax funding to operate and maintain facilities.

Roads and infrastructure

Road maintenance, transportation systems, and infrastructure improvements are largely funded through property taxes.

Emergency services

Fire departments, police services, and medical emergency response teams depend on government funding supported by tax revenue.

Public safety and community development

Community programs, public safety initiatives, and local development projects also rely on consistent tax income.

Why governments sell tax liens

When property owners fail to pay taxes, governments still need immediate revenue to fund these services. Instead of waiting indefinitely, they issue tax liens and sell them to investors to recover funds quickly and maintain financial stability.

A mutually beneficial system

This structure creates benefits for all parties involved:

- Governments receive immediate funding

- Property owners get time to repay their debt

- Investors earn interest through a government-regulated process

Educational systems like Tax Lien Wealth Builders help investors understand this government-backed structure in detail.

How property taxes create tax liens

Property taxes are assessed annually by local authorities based on property value and local tax rates. When these taxes go unpaid, the following process typically occurs:

- Tax bill is issued

- Payment deadline passes

- Property becomes delinquent

- Government records a tax lien

- Lien is prepared for auction

This process transforms unpaid taxes into investment opportunities through tax lien certificates.

To explore structured tax lien investment opportunities and educational resources, visit United Tax Liens.

How Property Tax Liens Work

Understanding how property tax liens function in the United States is essential for beginner investors. The system follows a structured legal and financial process designed to protect governments, property owners, and investors.

How property taxes are collected in the United States

Property taxes are collected at the local level, typically by counties or municipalities. Each year, property owners receive a tax bill based on assessed value and local tax rates.

Key features of property tax collection include:

- Annual billing cycles

- County-based administration

- Public tax records

- Legal enforcement mechanisms

- Penalties for non-payment

If taxes are paid on time, no further action occurs. If they are not, the delinquency process begins.

Explore real-world tax lien processes at United Tax Liens.

What happens when property taxes go unpaid

When property taxes go unpaid, local governments follow a legal process to recover funds.

This usually includes:

- Delinquency notice

- Penalty and interest addition

- Public record filing

- Tax lien creation

- Auction preparation

The government is not trying to take the property immediately. Instead, it aims to recover the unpaid tax revenue.

This structured approach reduces risk for investors because the lien is legally documented and enforceable.

The creation of a tax lien

The tax lien is officially created when the government records a legal claim against the property for unpaid taxes.

This claim includes:

- Unpaid tax amount

- Interest rate

- Penalties

- Legal filing details

- Redemption timeline

Once recorded, the lien becomes a public financial instrument that can be sold to investors.

This is where tax lien certificates enter the investment process.

Notice of tax lien explained

A notice of tax lien is a formal legal document informing the property owner and public that unpaid taxes exist and a lien has been placed on the property.

The notice typically includes:

- Property information

- Owner details

- Tax amount owed

- Interest rate

- Auction date

- Redemption period

This transparency allows investors to research liens before auctions.

To learn how to analyze notices and identify quality liens, visit MarketPlacePro.

Tax lien timeline from delinquency to auction

The tax lien timeline generally follows this structure:

- Property taxes due

- Payment missed

- Delinquency notice issued

- Lien recorded

- Public notice published

- Auction scheduled

- Investors bid on lien

- Certificate issued

The timeline varies by state, but the general process remains consistent across the United States.

Review investor education resources at United Tax Leans.

How Tax Lien Investing Works

Tax lien investing is the process of purchasing tax lien certificates and earning interest when property owners repay their unpaid property taxes. Instead of buying the property itself, investors buy the legal claim on the tax debt, which allows them to collect interest during the redemption period.

This system creates a structured investment opportunity backed by government regulations and county-level processes.

How investors buy tax liens

Investors purchase tax liens through county auctions or approved online tax lien platforms. These auctions are typically organized by local governments to recover unpaid property taxes quickly and efficiently.

The tax lien purchasing process

The process generally follows a clear and structured path:

- Researching available tax liens in selected counties

- Registering for county auctions or online platforms

- Reviewing lien details and property information

- Bidding on tax lien certificates

- Winning the lien at auction

- Receiving interest payments when the property owner redeems the lien

This structured approach makes tax lien investing more accessible than traditional real estate ownership, as investors do not need to manage tenants, maintain properties, or handle physical assets.

Start exploring opportunities

How counties sell tax lien certificates

Counties sell tax lien certificates to recover unpaid property taxes and maintain consistent funding for public services. Instead of waiting for property owners to pay, they transfer the tax debt to investors through a regulated auction system.

County tax lien sale process

The sale process typically includes several standardized steps:

- Public auction announcement

- Lien listing publication

- Investor registration and verification

- Competitive bidding process

- Certificate issuance to winning investors

This process creates a transparent and structured investment marketplace where investors can evaluate opportunities and participate in government-backed transactions.

How investors earn interest

The main source of profit in tax lien investing comes from interest payments made by property owners during the redemption period. When the property owner pays the outstanding taxes, they must also pay the interest and penalties attached to the lien.

Tax lien investor returns

When a lien is redeemed, the investor typically receives:

Interest rates vary by state and auction structure, usually ranging from 5% to 36% annually, making tax liens an attractive option for passive income investors looking for government-backed returns.

Redemption period explained

The redemption period is the legally defined timeframe during which property owners can repay unpaid taxes and remove the tax lien from their property. During this period, investors hold the certificate and earn interest on the outstanding debt.

Typical redemption timelines

Redemption periods vary by state and county but commonly range between:

- 6 months

- 1 year

- 2 years

- 3 years

During this time, the property owner maintains ownership while working to repay the tax debt, and the investor earns interest on the lien.

To understand redemption timelines by state, visit MarketPlacePro.

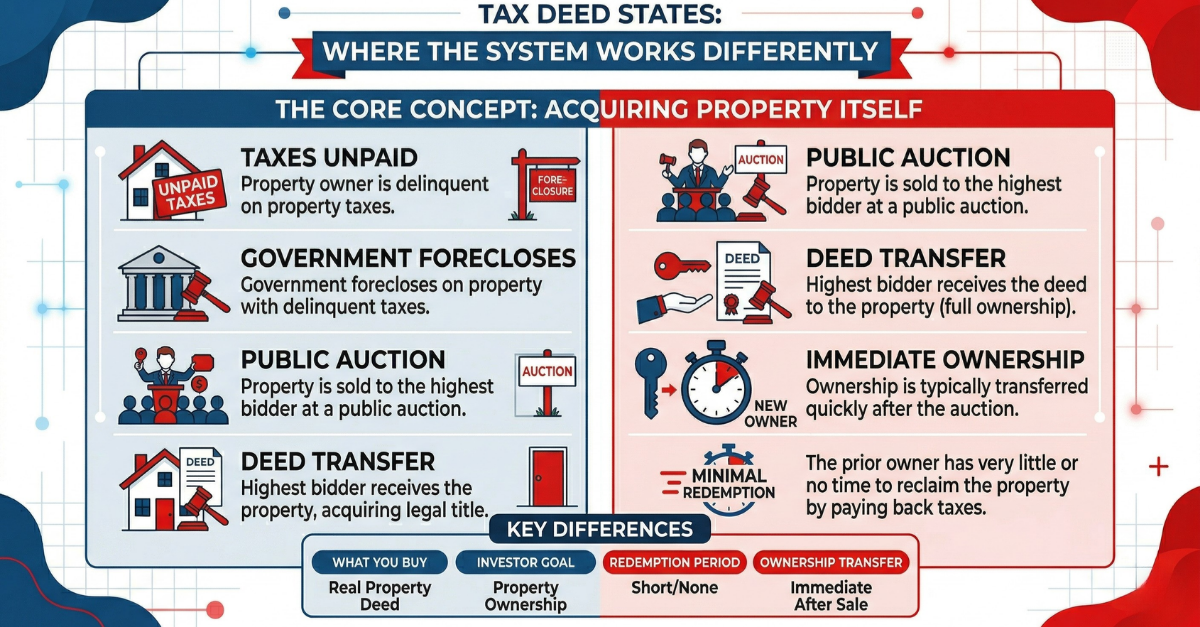

What happens if the owner does not pay

If the property owner does not repay the tax debt within the redemption period, the investor may gain the legal right to initiate foreclosure. This process allows the investor to pursue ownership of the property under state-specific regulations.

Possible outcomes for investors

Failure to redeem the lien can lead to several outcomes:

- Property ownership through foreclosure

- Tax deed acquisition in certain states

- Legal foreclosure proceedings

- Transfer of property title after court approval

However, foreclosure rules vary significantly by state and require strict legal compliance, proper documentation, and adherence to county procedures. Investors must understand local laws before pursuing this path to avoid legal complications.

Learn foreclosure strategies at Tax Lien Wealth Builders.

Tax Lien Certificates Explained

Tax lien certificates are the core financial instrument in tax lien investing. They represent the legal right to collect unpaid property taxes, along with interest and penalties, from property owners during the redemption period. Understanding how these certificates work is essential for investors who want to participate in tax lien auctions and build a structured investment strategy.

What is a tax lien certificate

A tax lien certificate is a legal document issued by a county or local government that proves an investor has purchased the unpaid tax debt associated with a property. Instead of buying the real estate itself, the investor buys the right to collect the outstanding taxes plus interest.

Information included in a tax lien certificate

A typical tax lien certificate contains several important details that define the investment:

- Property information and location

- Tax amount owed

- Interest rate set by the state or auction

- Redemption period timeline

- Auction and certificate issuance details

This certificate represents the investor’s legal claim to repayment and serves as official proof of the investment. As long as the property owner remains within the redemption period, the investor earns interest on the unpaid taxes.

Explore available certificates.

Tax lien certificate vs property ownership

One of the most common misunderstandings is that buying a tax lien certificate immediately grants property ownership. In reality, tax lien certificates do not transfer ownership at the time of purchase.

What investors actually receive

When purchasing a tax lien certificate, investors receive:

- A legal claim against the property for unpaid taxes

- The right to earn interest on the debt

- Potential foreclosure rights if the lien is not redeemed

Ownership only becomes possible if the property owner fails to repay the taxes within the redemption period and the investor follows the legal foreclosure process required by the state.

This distinction is important because tax lien investing is primarily an interest-based investment, not a direct real estate acquisition strategy.

Interest rates on tax liens

Interest rates on tax lien certificates vary significantly depending on state laws and auction structures. Each state sets maximum interest limits and bidding rules that determine how much investors can earn.

State interest rate examples

Some well-known examples include:

- Arizona: up to 16% interest

- Florida: up to 18% interest

- Illinois: up to 36% interest

- New Jersey: variable rate bidding system

These high potential returns make tax lien certificates attractive to investors seeking government-backed income opportunities with predictable interest structures.

Returns investors can expect

Tax lien investing can generate consistent returns, particularly for investors who conduct thorough research and select high-quality liens. While interest rates can be high, actual returns depend on several important factors.

Factors that affect investor returns

Typical annual returns range between 8% and 20%, depending on:

- State interest rate regulations

- Redemption speed (faster redemption may lower total return but increase liquidity)

- Auction competition and bidding strategy

- Quality of property and location research

Investors who focus on strong markets and structured bidding strategies often achieve more consistent and predictable results.

To learn how to identify high-return opportunities, visit United Tax Liens.

Risk level of tax lien certificates

Tax lien certificates are generally considered moderate-risk investments. While they are backed by government tax systems, they still require careful due diligence and strategic planning.

Common risks investors should understand

The main risks include:

- Poor property condition or low-value locations

- Legal and foreclosure complexity

- Uncertain redemption timelines

- Increased market competition in popular counties

Proper education, research, and platform support can significantly reduce these risks and help investors make informed decisions. Understanding state laws, property data, and auction dynamics is essential for building a sustainable tax lien investment strategy.

Tax Lien Auctions and Sales

Tax lien auctions are the primary way investors acquire tax lien certificates. These public sales allow counties to recover unpaid property taxes while giving investors the opportunity to earn interest through government-regulated processes. Understanding how auctions work is essential for anyone entering the tax lien investing market.

How tax lien auctions work

Tax lien auctions are public sales where investors bid on tax liens issued by counties or municipalities. The goal of the auction is to transfer the unpaid tax debt from the government to investors who are willing to pay the outstanding taxes in exchange for interest and legal claim rights.

Auction structure and bidding process

In most tax lien auctions, investors compete by offering the most favorable terms according to the county’s rules. The winning bidder is determined either by the lowest interest rate offered or the highest premium paid for the lien.

The general auction process includes:

- County publishes tax lien listings

- Investors register for the auction

- Bidding takes place online or in person

- Winning bidders receive tax lien certificates

- Investors earn interest during the redemption period

This structured system ensures transparency and fairness while allowing counties to recover funds quickly.

View auction preparation resources at MarketPlacePro.

Online vs in-person tax lien auctions

Tax lien auctions can take place either online or in person, depending on the county and state regulations. Both formats offer unique advantages and challenges for investors.

Online tax lien auctions

Online auctions have become increasingly popular because they allow investors to participate from anywhere in the country. These platforms provide access to multiple counties, digital property data, and streamlined registration processes.

Key benefits include:

- Convenience and remote participation

- Access to multiple markets

- Faster bidding and data availability

- Lower travel and logistical costs

In-person tax lien auctions

In-person auctions still exist in some counties and offer advantages that online platforms cannot fully replicate.

Benefits include:

- Local market insights and networking

- Direct interaction with county officials

- Reduced digital competition in some areas

- Better understanding of local property conditions

Many counties now use hybrid or fully online platforms to increase participation and efficiency.

External reference:

[EXTERNAL LINK: County Tax Sale Portal]

Bid down interest vs premium bidding

Different counties use different auction formats, and understanding these structures is critical for calculating potential returns.

Bid down interest auctions

In bid down interest auctions, investors compete by offering the lowest interest rate they are willing to accept. The investor who accepts the lowest interest rate wins the tax lien certificate.

This format reduces returns but increases the likelihood of winning in competitive markets.

Premium bidding auctions

In premium bidding auctions, investors bid by offering additional money above the tax debt. The highest premium bidder wins the lien, and the interest rate is typically fixed by the state.

This format can reduce overall returns because the premium paid may not always be recoverable.

Each auction format affects profitability, risk, and investment strategy differently.

How to prepare for a tax lien auction

Preparation is one of the most important steps in tax lien investing. Investors who enter auctions without research or planning often face unnecessary risks and lower returns.

Key preparation steps

Before participating in an auction, investors should focus on:

- Property research and valuation

- Title and lien review

- County rules and auction structure analysis

- Budget planning and bidding limits

- Risk assessment and exit strategy

Proper preparation helps investors avoid low-value properties and identify high-quality opportunities.

Prepare with Tax Lien Wealth Builders.

Research before bidding

Research is the most critical factor in successful tax lien investing. Experienced investors spend significant time analyzing properties and legal conditions before placing any bids.

What investors should analyze

A strong research process includes:

- Property location and neighborhood quality

- Estimated market value

- Property condition and land use

- Legal status and ownership records

- Existing liens, mortgages, or code violations

Thorough research reduces risk and increases the chances of selecting liens that will redeem quickly and generate consistent returns.

For detailed research frameworks and step-by-step analysis methods, visit United Tax Liens.

Federal Tax Liens and Government Liens

Understanding federal tax liens and government liens is essential for tax lien investors because these legal claims can affect lien priority, foreclosure rights, and repayment order. While most tax lien investing focuses on local property tax liens, federal tax liens issued by the government can influence how and when investors get paid.

Tax lien federal meaning

A federal tax lien is a legal claim issued by the Internal Revenue Service (IRS) when a taxpayer fails to pay federal taxes. This lien protects the government’s right to collect unpaid taxes by placing a claim on the taxpayer’s assets.

Unlike local property tax liens, federal tax liens apply to a broader range of assets and can impact investment outcomes.

External reference:

[EXTERNAL LINK: IRS Federal Tax Lien Guide]

IRS tax liens explained

IRS tax liens are applied automatically after the government assesses unpaid taxes and sends a demand for payment. If the taxpayer does not resolve the debt, the IRS files a public notice of federal tax lien.

Assets affected by IRS tax liens

Federal tax liens can apply to:

- Real estate and land

- Personal property

- Financial accounts

- Business assets

- Future acquired assets

This makes federal tax liens broader in scope than property tax liens, which are limited to a specific property.

Federal tax lien vs property tax lien

Federal tax liens and property tax liens serve different purposes and operate under different legal frameworks.

Property tax liens

- Issued by counties or municipalities

- Apply to a specific property

- Often sold to investors at auctions

- Typically hold priority in repayment

Federal tax liens

- Issued by the IRS

- Apply to all taxpayer assets

- Not sold to investors

- Can affect foreclosure and repayment order

This distinction is important because tax lien investors must understand how federal claims interact with local tax liens.

When federal tax liens affect investors

Federal tax liens can impact investors when multiple claims exist on the same property. In these cases, the order of repayment becomes critical.

Impact on tax lien investments

Federal tax liens may:

- Delay foreclosure processes

- Affect repayment timelines

- Require additional legal steps

- Influence lien priority decisions

Investors must carefully review lien records and title reports before bidding to ensure no unexpected federal claims exist.

Priority of liens

Lien priority determines which creditor gets paid first when a property is sold or foreclosed. This is one of the most important legal concepts in tax lien investing.

How lien priority works

In most cases:

- Property tax liens hold first priority

- Federal tax liens come after local tax liens

- Mortgages and other debts follow

This priority structure often protects tax lien investors, but federal involvement can still complicate foreclosure procedures and timelines.

Learn legal priority rules at MarketPlacePro.

Tax Lien vs Levy

Understanding the difference between a tax lien and a tax levy is essential because these terms are often confused, yet they represent very different legal actions.

What is a tax levy

A tax levy is the legal seizure of property or assets to satisfy unpaid tax debt. While a lien represents a claim, a levy is the enforcement action that allows the government to take assets directly.

Levy vs lien explained

The difference between a lien and a levy can be summarized simply.

Tax lien

- Legal claim on property

- Protects the government’s right to collect

- Does not seize assets immediately

- Can be sold to investors (property tax liens)

Tax levy

- Seizure of assets or property

- Enforces payment of tax debt

- Removes control from the taxpayer

- Used by government agencies

Difference between lien and levy

A lien is a protective legal measure, while a levy is an enforcement action.

Legal function of each

- A lien secures the government’s financial claim

- A levy forces payment through asset seizure

- A lien creates investment opportunities

- A levy resolves debt through enforcement

This distinction helps investors understand why tax liens are investment tools while tax levies are enforcement mechanisms.

Lien or levy meaning in legal terms

Legal definitions vary slightly by jurisdiction, but the core concept remains consistent: liens protect claims, while levies enforce collection.

Which one affects investors more

Tax liens directly affect investors because they create opportunities to purchase certificates and earn interest. Levies, on the other hand, are government enforcement actions and are not part of tax lien investment strategies.

Understand legal differences at United Tax Liens.

Tax Lien Laws and Legal Framework

Tax lien investing operates within a strict legal framework governed primarily by state laws and county regulations. Investors must understand these legal structures to avoid compliance issues and protect their investments.

Tax lien law in the United States

Tax lien laws are determined at the state level, meaning each state has its own rules for auctions, redemption periods, interest rates, and foreclosure procedures.

State-by-state tax lien regulations

Because regulations vary, investors must research each state carefully before participating in auctions.

Key legal differences between states

- Interest rate limits

- Redemption periods

- Auction formats

- Foreclosure processes

- Certificate validity periods

These variations create different risk and return profiles across markets.

Redemption periods and legal timelines

Redemption periods define how long property owners have to repay their taxes and remove the lien.

Timeline variations

- Short redemption periods increase investor liquidity

- Long redemption periods increase total interest potential

- State laws define exact timelines

Understanding these timelines helps investors plan their capital and expected returns.

Foreclosure rights

Foreclosure rights allow investors to take legal action if the property owner fails to repay the tax debt.

Legal foreclosure process

The process may include:

- Filing legal notices

- Court approval

- Waiting periods

- Title transfer procedures

Since foreclosure rules vary widely, investors must follow state-specific legal procedures carefully.

Compliance and legal risks

Legal compliance is critical in tax lien investing. Failure to follow state laws can result in lost investments or legal complications.

Common compliance risks

- Incorrect notice filings

- Missed deadlines

- Improper foreclosure procedures

- Incomplete documentation

Careful legal review and proper education reduce these risks significantly.

Benefits of Tax Lien Investing

Tax lien investing offers several advantages that make it attractive to both new and experienced investors. These benefits come from the structured, government-backed nature of the tax lien system.

Passive income potential

Tax lien certificates generate interest income when property owners repay their taxes. This allows investors to earn returns without managing physical real estate or dealing with tenants.

Consistent interest-based returns

Investors can receive:

- Fixed interest payments

- Predictable redemption returns

- Government-regulated income structures

This makes tax lien investing appealing for passive income strategies.

Real estate-backed security

Tax lien certificates are backed by real property, which adds an extra layer of security compared to many financial investments.

Property-backed protection

Because the lien is attached to real estate:

- The investment is secured by land or property

- Foreclosure rights may exist

- Government enforcement supports repayment

This structure reduces some of the risks associated with unsecured investments.

High interest rates

Tax lien certificates often offer higher interest rates than traditional fixed-income investments such as bonds or savings accounts.

Competitive returns

Interest rates may exceed:

- Bank savings rates

- Government bonds

- Some real estate income strategies

This makes tax liens attractive for yield-focused investors.

Portfolio diversification

Tax lien investing helps diversify real estate and financial portfolios by adding a government-backed asset class.

Diversification benefits

Investors can:

- Spread capital across multiple properties

- Invest in different counties or states

- Reduce dependence on traditional real estate

Diversification helps balance risk and improve long-term stability.

Lower capital requirements

Tax lien investing allows investors to start with smaller budgets compared to traditional real estate purchases.

Accessible entry point

Investors can:

- Buy individual certificates

- Invest in multiple small liens

- Scale gradually over time

This makes tax lien investing accessible to beginners and experienced investors alike.

Start building your portfolio.

Risks of Tax Lien Investing

While tax lien investing offers attractive returns and government-backed security, it is not risk-free. Investors must understand the potential downsides before participating in auctions or purchasing certificates. Identifying these risks early helps investors build safer strategies and protect their capital.

Talk to a United Tax Liens coach before you bid

Property condition risks

One of the most common risks in tax lien investing is the condition and value of the underlying property. Since investors are buying the tax debt and not physically inspecting every property, some liens may be tied to low-value or undesirable assets.

Low-value or problematic properties

Some properties associated with tax liens may include:

- Vacant land with little market demand

- Abandoned or damaged buildings

- Properties in declining neighborhoods

- Landlocked or inaccessible lots

If foreclosure becomes necessary, these properties may not provide sufficient value to justify the investment. This is why property research is a critical step before bidding.

Redemption uncertainty

Tax lien returns depend heavily on whether and when the property owner redeems the lien. While many liens do redeem, the timing can vary significantly.

Unpredictable redemption timelines

Investors may face:

- Delayed redemption periods

- Long waiting times for interest payments

- Uncertainty in cash flow

- Extended capital lock-in

Some liens redeem quickly, while others may take years, affecting liquidity and investment planning.

Legal and compliance risks

Tax lien investing operates under strict legal frameworks, and mistakes in compliance can lead to financial losses or legal complications.

Legal mistakes that can affect investors

Common compliance risks include:

- Missing legal deadlines

- Improper foreclosure procedures

- Incorrect notice filings

- Failure to follow state regulations

Investors who do not fully understand the legal process may lose their lien rights or face costly legal issues. Proper education and structured guidance help reduce these risks.

Market and auction competition

As tax lien investing becomes more popular, competition at auctions has increased. More investors bidding on the same liens can reduce potential returns.

Impact of competition

Higher competition can lead to:

- Lower interest rates in bid-down auctions

- Higher premiums in competitive markets

- Fewer high-quality liens available

- Reduced overall profitability

Careful market selection and research help investors avoid overly competitive counties.

Illiquidity

Tax lien certificates are not highly liquid investments. Unlike stocks or bonds, they cannot be easily sold or converted into cash.

Limited resale options

Investors may experience:

- Capital tied up during redemption periods

- Limited secondary markets

- Long holding periods

- Restricted exit strategies

Because of this, tax lien investing is generally considered a medium- to long-term investment.

Learn risk management at Tax Lien Wealth Builders.

Best States for Tax Lien Investing

Choosing the right state is one of the most important decisions in tax lien investing. Different states offer different interest rates, redemption periods, and auction structures, which directly affect returns and risk levels.

Arizona

Arizona is often considered one of the most investor-friendly tax lien states due to its structured auction system and clear legal framework.

Key advantages of Arizona

- Interest rates up to 16%

- Transparent bidding process

- Well-organized county auctions

- Strong legal structure

This makes Arizona a popular starting point for many investors.

Florida

Florida is known for its online auction systems and predictable redemption timelines, making it accessible for remote investors.

Why investors choose Florida

- Fully online auctions in most counties

- Up to 18% interest rates

- Regular auction schedules

- Large number of available liens

Florida offers a balance between accessibility and stable returns.

Illinois

Illinois stands out for its high potential returns and unique penalty-based system.

Investment benefits

- Interest rates up to 36%

- Strong redemption rates

- High return potential

- Structured legal process

However, competition can be intense in popular counties.

New Jersey

New Jersey uses a premium bidding system that creates a different investment dynamic.

Auction structure

- Premium bidding format

- Fixed interest rates

- Foreclosure opportunities

- Strong legal protections

This system can be beneficial for experienced investors who understand premium strategies.

Other tax lien states

Many other states also offer tax lien opportunities, each with unique legal and financial structures.

Additional markets to explore

- Colorado

- Iowa

- Maryland

- Georgia (redeemable deeds)

- South Carolina

Exploring multiple states allows investors to diversify and find less competitive opportunities.

Explore state guides at MarketPlacePro.

Beginner Strategies for Tax Lien Investing

New investors should focus on simple and structured strategies to reduce risk and build experience gradually. A disciplined approach increases the chances of long-term success.

Explore our blog for step-by-step guides

Start with research

Research is the foundation of successful tax lien investing. Understanding property data, county rules, and market conditions helps investors avoid poor-quality liens.

Key research areas

- Property location and value

- County regulations

- Redemption rates

- Auction structure

- Legal requirements

Thorough research improves decision-making and reduces costly mistakes.

Focus on low-risk counties

Beginners should start with stable counties that have strong redemption rates and clear legal processes.

Characteristics of low-risk counties

- Stable real estate markets

- High redemption rates

- Transparent auction systems

- Predictable legal timelines

This approach helps investors build confidence and experience.

Build a diversified lien portfolio

Diversification is one of the safest strategies in tax lien investing.

Benefits of diversification

- Reduced exposure to single-property risk

- More consistent redemption outcomes

- Balanced returns across multiple liens

- Improved capital stability

Spreading investments across different properties and counties reduces overall risk.

Understand redemption periods

Redemption timelines directly affect how quickly investors receive returns.

Timing considerations

- Short redemption periods improve liquidity

- Long redemption periods increase interest potential

- State laws determine timelines

Understanding this balance helps investors plan their cash flow.

Work with experienced platforms

Using reliable platforms and structured systems can simplify the investment process and reduce legal risks.

Benefits of professional platforms

- Verified lien data

- Market insights

- Legal compliance support

- Structured investment tools

Start with Tax Lien Wealth Builders.

How Tax Lien Investing Fits in a Real Estate Portfolio

Tax lien investing can play a valuable role in a broader real estate investment strategy by providing income, diversification, and risk balance.

Alternative investment strategy

Tax liens serve as an alternative to traditional real estate ownership by focusing on debt rather than property management.

Complementing real estate holdings

They can be used alongside:

- Rental properties

- Commercial real estate

- REIT investments

- Land investments

This creates a more balanced portfolio.

Passive income component

Tax liens generate interest-based income without requiring property maintenance or tenant management.

Income advantages

- Predictable interest payments

- Government-backed structure

- Reduced operational involvement

This makes them suitable for passive income strategies.

Risk balancing

Tax liens help balance risk by adding a different type of real estate exposure.

Portfolio stability benefits

- Less exposure to market fluctuations

- Diversified income streams

- Reduced dependence on property appreciation

Long-term investment planning

Tax lien investing supports long-term financial planning by providing steady returns and structured growth opportunities.

Build your strategy with Tax Lien Wealth Builders.

Frequently Asked Questions About Tax Liens

How do you get a tax lien

Investors obtain tax liens by participating in county tax lien auctions or using approved online platforms that list available certificates.

Are tax liens safe

Tax liens are relatively secure because they are backed by government tax systems and real estate, but they still require proper research and due diligence.

Can you lose money in tax lien investing

Yes, losses can occur if investors purchase liens tied to low-value properties, fail to follow legal procedures, or overpay during competitive auctions.

How much money do you need

Some tax lien certificates start at under $500, making them accessible to investors with smaller budgets.

Can beginners invest in tax liens

Yes, beginners can invest in tax liens successfully if they focus on education, research, and structured investment strategies.

Read investor experience.

Final Thoughts on Tax Lien Investing

Tax lien investing offers a structured and educational entry point into real estate-backed investments for beginner retail investors. With government-backed legal frameworks, predictable interest rates, and relatively low capital requirements, tax lien certificates can serve as a valuable component of a diversified investment portfolio.

However, success in tax lien investing depends on education, research, and strategic execution. Investors who understand redemption periods, state laws, auction systems, and property research methods are far more likely to generate consistent returns and avoid common risks.

Educational platforms like Tax Lien Wealth Builders, MarketPlacePro., and Unified Wealth System provide structured guidance, while Unified Tax Liens (UTL) offers practical access to opportunities and resources for investors looking to enter this market responsibly.

If you are ready to explore tax lien investing opportunities, review available resources and investor feedback.

Get started with United Tax Liens today.

This pillar guide is designed to serve as a long-term educational resource and starting point for beginners entering the tax lien investment space.