If you have spent any time researching delinquent property tax investing, you have almost certainly come across the terms tax lien states and tax deed states. These terms describe two fundamentally different systems that governments use to recover unpaid property taxes, and the investment model that flows from each one is equally different.

Many beginners assume these two paths are variations of the same strategy. They are not. Buying a tax lien certificate is a debt-based investment that generates interest income. Buying a tax deed means you are acquiring direct ownership of a property. The capital requirements, risk profiles, due diligence processes, and exit strategies are distinct enough that confusing the two before your first auction can lead to costly mistakes.

This guide explains both systems clearly, compares them across every dimension that matters to investors, and helps you determine which path fits your goals. If you want to explore what structured tax lien investing looks like in practice before reading further, the team at United Tax Liens works specifically with investors in the tax lien certificate model.

What Are Tax Lien States?

In a tax lien state, when a property owner fails to pay their property taxes, the local government does not immediately take the property. Instead, it places a legal claim against it called a tax lien and sells that claim to private investors at a public auction.

The investor pays the outstanding tax debt to the government and receives a tax lien certificate in return. That certificate entitles the investor to collect the original tax amount plus interest and penalties when the property owner eventually repays the debt. The property owner retains ownership during this period and has a legally defined window of time called the redemption period to pay back what is owed.

If the owner fails to repay within the redemption period, the certificate holder may gain the right to initiate foreclosure proceedings and potentially acquire the property through a legal process. However, the primary investment thesis in tax lien states is interest income, not property acquisition. Most certificates redeem without ever reaching foreclosure.

How the Tax Lien Certificate Model Works

The mechanics of tax lien investing follow a structured sequence that is consistent across most tax lien states, with variation in specific rates, timelines, and auction formats.

- Property owner fails to pay property taxes by the due date

- Local government records a tax lien against the property

- County schedules a public auction to sell the lien to investors

- Investor purchases the certificate by paying the outstanding tax debt

- Investor earns interest at the state-defined rate during the redemption period

- Property owner repays the debt and the investor receives principal plus interest

- If the owner does not pay, the investor may pursue foreclosure rights

This model is what platforms like United Tax Liens are built around — helping investors participate in the certificate market with structured research, coaching, and operational support.

Key Characteristics of Tax Lien States

- Investor purchases a debt claim, not the property itself

- Returns are generated through interest and penalties during the redemption period

- Capital requirements are typically lower than direct property acquisition

- No property management responsibilities during the certificate holding period

- Foreclosure is a possible but secondary outcome, not the primary investment goal

Primary tax lien states include Arizona, Florida, Illinois, New Jersey, Indiana, Iowa, Colorado, Maryland, Nebraska, and several others. For a full breakdown of which states operate this way, the United Tax Liens blog covers state classification in detail.

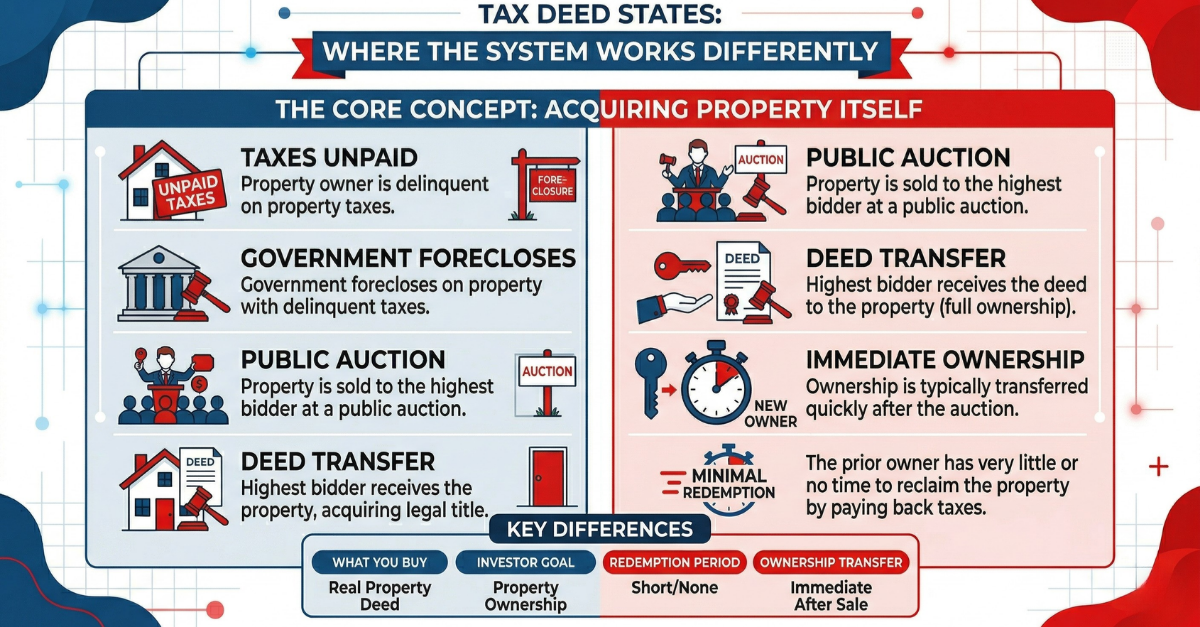

What Are Tax Deed States?

In a tax deed state, the government takes a more direct approach to recovering unpaid property taxes. Instead of selling the debt to investors, the government waits until the delinquency reaches a legal threshold, seizes the property from the owner, and then auctions the property itself to the highest bidder.

The investor in a tax deed state is buying the property outright, not a certificate against it. This means the investment requires significantly more capital, involves direct real estate ownership from day one, and carries a completely different due diligence burden. There is no redemption period in the traditional sense — once the deed is transferred, the original owner typically has limited or no recourse.

How Tax Deed Sales Work

The tax deed process follows a different sequence from the lien model, and the investor's role in that process is fundamentally different.

- Property owner fails to pay property taxes for an extended delinquency period

- Government initiates a legal process to seize the property

- County schedules a tax deed auction for the seized property

- Investors bid on the property itself, with the highest bid winning

- Winning bidder receives a tax deed transferring ownership of the property

- Investor now owns the property and must manage, sell, or develop it

The investor in a tax deed auction is making a real estate acquisition decision, not a debt investment decision. The research required, the capital deployed, and the post-purchase responsibilities are all significantly more complex than holding a tax lien certificate.

Key Characteristics of Tax Deed States

- Investor purchases the property directly at auction

- Returns come from resale, rental income, or property development

- Capital requirements are substantially higher than tax lien certificate investing

- Immediate property management or disposition responsibility upon winning

- Title issues and property condition risks are absorbed by the buyer

Primary tax deed states include California, Michigan, Minnesota, Nevada, New York, Oregon, Washington, and Wisconsin, among others. Some of these states conduct what are called over-the-counter sales for properties that did not sell at auction, which can offer additional acquisition opportunities for real estate investors.

Not sure which investment model fits your situation? Talk to a United Tax Liens coach to get a direct answer based on your goals, capital, and timeline.

Hybrid States: Redeemable Tax Deeds

A third category exists that many investors overlook: states that use a hybrid system called redeemable tax deeds. These states combine elements of both the lien and deed models in a way that creates a distinct investment dynamic.

In a redeemable deed state, the investor purchases a deed to the property at auction — similar to a tax deed state — but the original property owner retains the right to reclaim the property within a defined redemption period by paying the purchase price plus a penalty or premium. This redemption right means the investor does not immediately have full, unchallenged ownership.

How Redeemable Deed States Work

The process in a redeemable deed state sits between a pure lien state and a pure deed state.

- Government auctions the property after a delinquency period

- Investor wins the auction and receives a deed to the property

- Original owner has a redemption window — typically six months to two years — to buy back the property

- If the owner redeems, the investor receives their purchase price plus the redemption penalty

- If the owner does not redeem, the investor retains full ownership of the property

Georgia and Texas are the two most prominent redeemable deed states. Georgia has a one-year redemption period with a 20% premium penalty. Texas has a redemption period that varies by property type with penalties that can reach 25% or more.

What Makes Redeemable Deeds Different from Both Systems

Redeemable deeds carry more risk than pure tax lien certificates because the investor is taking on a form of property ownership from the moment of purchase. Title issues, property condition problems, and encumbrances can all affect the investment in ways that a simple certificate would not. At the same time, the penalty-based return structure can generate attractive short-term returns if the owner redeems quickly.

Investors interested in redeemable deed markets should approach them with the due diligence standards of real estate acquisition, not the lighter research burden appropriate for certificate investing. The Tax Lien Wealth Builders blog covers the strategic differences between certificate and deed investing for investors who want to understand both models before choosing.

Tax Lien vs Tax Deed: A Direct Comparison

The following comparison covers every dimension that matters to investors evaluating these two systems. Understanding each factor helps you make a decision based on your actual situation, not on which name sounds more appealing.

Capital Requirements

Tax lien certificates can often be purchased for a few hundred dollars in lower-value markets, and even certificates in mid-range counties rarely require the same upfront capital as purchasing a property outright. The entry point for tax deed investing is the property's auction price, which typically reflects a discount to market value but still requires significantly more capital per investment.

For investors with limited starting capital who want to diversify across multiple positions, the tax lien certificate model offers a much lower barrier to entry. United Tax Liens works with investors across different capital levels and can help structure a realistic starting portfolio.

Risk Profile

Tax lien certificates carry risk primarily around property quality and legal compliance. If the property underlying a certificate is worthless — a condemned structure, a landlocked lot, a property with environmental contamination — and the owner never redeems, the investor may end up holding a certificate against an asset that produces no recovery value even after foreclosure.

Tax deed investing carries all of those risks plus the additional complexity of direct ownership: title defects that survive the tax sale, property condition issues, existing occupants who may need to be evicted, and carrying costs during the period before resale or development. The due diligence burden in a tax deed state is substantially higher.

Return Structure

Tax lien certificates generate returns through interest payments at state-regulated rates, typically ranging from 8% to 36% annually depending on the state and auction outcome. The return is predictable in structure even if variable in rate.

Tax deed investing generates returns through property resale, rental income, or development. The upside can be higher than certificate interest rates in the right market, but the variability is also much greater. A property purchased at a tax deed auction may need significant rehabilitation before it can be sold or rented, which adds cost and time to the return equation.

Investors who want the predictability of interest-based returns with government-backed legal structure generally prefer the tax lien model. Those who are comfortable with direct real estate ownership and the associated complexity may find tax deed opportunities more suitable. The United Tax Liens services page outlines how the certificate model generates returns at each stage of the investment cycle.

Due Diligence Requirements

Research in both systems starts with the property, but the depth of investigation required differs significantly.

For tax lien certificates, investors need to verify that the underlying property has enough value to justify the certificate cost if foreclosure becomes necessary. This means checking estimated market value, basic property condition, and the presence of any superior liens that would survive or complicate the investment. For most certificates that redeem normally, even modest due diligence is sufficient.

For tax deed purchases, the due diligence requirement is much closer to a full real estate acquisition. Investors need to assess title clarity, physical condition, existing occupants, zoning restrictions, environmental issues, and local market conditions for resale. Skipping any of these steps in a tax deed auction can mean inheriting major problems with the property.

Time Commitment

Holding a tax lien certificate is largely passive. Once the certificate is purchased and any required maintenance payments are made, the investor waits for redemption. There are no tenants to manage, no property maintenance to coordinate, and no active decisions to make until either the certificate redeems or the foreclosure process begins.

Tax deed ownership is active from day one. The investor either needs to manage the property, coordinate rehabilitation, or list it for resale — all of which require ongoing time and decision-making. This is a meaningful distinction for investors who are looking for passive income rather than another active real estate management responsibility.

For investors specifically looking for a more passive income structure, reading about how other investors have experienced the tax lien model can help set realistic expectations about the actual time commitment involved.

Legal Complexity

Both systems involve legal complexity, but of different kinds. Tax lien certificate investing requires understanding and complying with state-specific rules around notice requirements, certificate maintenance, and foreclosure procedures. Getting these wrong can cost you the certificate or the foreclosure right.

Tax deed investing introduces additional legal risks around title. Properties sold at tax deed auctions are often sold with a tax deed rather than a warranty deed, which means the government is not guaranteeing the title is clean. Investors may discover after purchase that the property carries liens, judgments, or other encumbrances that were not extinguished by the tax sale. Title insurance is often unavailable or limited for tax deed purchases, adding to the legal risk.

The United Tax Liens coaching team helps investors understand the specific legal requirements in their target states so compliance errors do not undermine otherwise sound investments.

Want to understand the legal requirements in your target state before you invest? Explore the United Tax Liens services page to see how structured support helps investors stay compliant from day one.

Which System Is Right for You?

The answer depends on four things: your available capital, your risk tolerance, how much time you want to spend managing your investments, and what kind of return structure you are looking for.

Choose Tax Lien Investing If:

- You are starting with limited capital and want to diversify across multiple positions

- You want predictable, interest-based returns rather than variable real estate appreciation

- You prefer a passive investment structure without property management responsibilities

- You are new to real estate investing and want a lower-complexity entry point

- You want government-backed legal structure protecting your investment position

The tax lien certificate model is designed specifically for investors who match this profile. United Tax Liens provides the research tools, coaching support, and structured guidance that helps investors in this category build a functioning portfolio without having to figure out everything independently.

Choose Tax Deed Investing If:

- You have sufficient capital to purchase properties outright at auction prices

- You have experience with real estate acquisition, rehabilitation, and resale

- You are comfortable managing properties or coordinating with contractors and property managers

- You are looking for equity upside rather than interest income

- You have the capacity to conduct thorough title and property condition research before bidding

Tax deed investing is closer to traditional real estate acquisition than it is to the interest-income model of tax lien certificates. Investors who are already active in real estate and want to source discounted properties through the tax deed channel may find it complements their existing skill set. Tax Lien Wealth Builders offers educational resources that help investors understand both models before committing to either.

Consider Redeemable Deed States If:

- You want the potential for property acquisition but with a defined redemption window that generates a return even without taking ownership

- You are experienced with real estate due diligence and understand the title risks involved

- You are targeting markets like Georgia or Texas where the redeemable deed model is well-established

- You have the capital to purchase at auction and hold the property through the redemption period if needed

Redeemable deed states offer a middle path, but they require a more sophisticated investor who understands the nuances of both systems. The Tax Lien Wealth Builders services page includes resources on evaluating hybrid markets for investors who want to explore that option.

Common Misconceptions About Tax Lien and Tax Deed Investing

Misconception 1: Tax Lien Investing Guarantees You Will Get the Property

Most tax lien certificates redeem without ever reaching foreclosure. The majority of property owners pay their delinquent taxes before the redemption period expires. Investors who enter the tax lien market expecting to routinely acquire properties through foreclosure will often be disappointed. The primary return mechanism is interest income on the certificate, not property acquisition.

That said, foreclosure does happen when owners cannot or do not pay. Understanding the foreclosure process in your target state is important even if you never expect to use it. A United Tax Liens coach can walk you through exactly how foreclosure works in the states you are considering.

Misconception 2: Tax Deed Investing Is Always Cheaper Than Buying Normally

Tax deed auctions do sometimes produce properties at significant discounts to market value. But the discount has to be understood in context. Properties sold at tax deed auctions often have deferred maintenance, unclear title, or other issues that reduce their actual value. Competition at auction in popular markets can also drive prices close to or even above comparable retail values for desirable properties.

The discount at a tax deed auction is real in the right circumstances, but it is not guaranteed and it is not automatic. Thorough research before bidding is what separates investors who find genuine value from those who overpay for a problem property.

Misconception 3: You Can Ignore Due Diligence If the Price Is Low

This misconception affects both systems. In tax lien investing, a cheap certificate tied to a worthless property is still a bad investment. In tax deed investing, a low auction price does not compensate for a property with title defects, environmental issues, or structural problems that cost more to resolve than the discount provides.

Due diligence is not optional in either system. The United Tax Liens blog regularly publishes research frameworks that help investors evaluate properties before committing capital at auction.

Misconception 4: These Systems Are the Same Everywhere

State and county-level rules create enormous variation in how both systems actually operate. A Florida tax lien auction is conducted entirely online. An Illinois auction may require in-person attendance. A Georgia redeemable deed carries specific redemption penalties that differ from Texas. Treating any state's rules as interchangeable with another's is a reliable way to make compliance errors.

Always research the specific rules for each state and county you plan to invest in. Tax Lien Wealth Builders covers state-specific rules in its educational content for investors who want current, actionable information.

Getting Started: Practical Next Steps

Once you have decided which model fits your situation, the path to your first investment follows a consistent sequence regardless of which system you choose.

Step 1: Confirm Your State's Classification

Before researching counties or individual opportunities, verify that your target state is actually a tax lien state, a tax deed state, or a hybrid. This single step prevents wasted research effort and ensures you are using the right due diligence framework from the start. United Tax Liens provides state classification information as part of its investor onboarding resources.

Step 2: Learn the Specific Rules for Your Target State

Interest rates, redemption periods, auction formats, notice requirements, and foreclosure procedures all vary by state. Investing in a state you do not understand operationally is the most common source of avoidable losses in both tax lien and tax deed investing. Take the time to understand the rules before the auction, not after.

Step 3: Build a Property Research Process

Whether you are buying a certificate or a deed, the quality of your property research determines the quality of your outcomes. Develop a consistent checklist that covers property value, condition, title status, and any competing claims before you commit capital to any investment.

Investors who work with United Tax Liens get access to structured research frameworks that systematize this process and reduce the risk of missing critical information before a bid.

Step 4: Start Small and Build Experience

In tax lien investing, this means targeting smaller certificates in less competitive counties on your first few auctions. In tax deed investing, it means starting with lower-priced properties in markets you understand before scaling up. Experience in the auction environment itself is valuable and cannot be fully replicated through research alone.

Step 5: Connect With Structured Support

Both systems reward investors who have access to good information, legal guidance, and market knowledge. Going fully independent from day one is possible, but it extends the learning curve and increases the probability of early mistakes. Educational programs like Tax Lien Wealth Builders and platforms like United Tax Liens are designed to shorten that curve significantly.

Ready to move from research to your first investment? Visit the United Tax Liens services page to explore how structured coaching and research support helps investors get started with confidence.

Final Thoughts: Tax Lien vs Tax Deed

Tax lien states and tax deed states represent two different paths into the delinquent property tax investing space. They share a common origin — unpaid property taxes — but diverge significantly in what the investor actually buys, how returns are generated, and what risks are involved.

Tax lien certificate investing is a debt-based, interest-income model. It is more accessible, more passive, and lower in capital requirements than direct property acquisition. The legal framework is government-backed and the return structure is predictable. For investors who are new to real estate investing, looking for passive income, or working with limited starting capital, it is generally the more appropriate entry point.

Tax deed investing is a property acquisition model. It offers the potential for equity upside and significant discounts on real estate, but it requires more capital, more due diligence, more active management, and a higher tolerance for legal and property condition risk. It is better suited to investors who already have real estate experience and want to add a distressed property channel to an existing strategy.

Redeemable deed states occupy a middle ground that can work well for experienced investors who understand both models, but they are not the right starting point for beginners.

If the tax lien certificate model matches your goals, United Tax Liens is a platform built specifically to support investors in that space — from market selection through certificate management and beyond. For broader educational content on both systems, the Tax Lien Wealth Builders blog is one of the most comprehensive resources currently available for self-directed investors.

Take the next step toward your first tax lien investment. Contact the United Tax Liens team today and get personalized guidance on the market, strategy, and first steps that fit your situation.